Analysis – How small will smaller be? Week 25 Update

Paris, June 24th – “We will come back smaller“. This is probably one the most common assertions we have been hearing from airlines CEOs over the past weeks. But how small will smaller actually be? Low visibility and daily changes in the global spread of Covid19 make it quite difficult to navigate through this question. Data on early signs of recovery in Europe, however, bring some material for reflection.

The scope of this analysis has been limited to the 3 main diversified airline groups in Europe, holding both legacy and low-cost operations, as well as medium and long-haul flights.

Week 25 Update

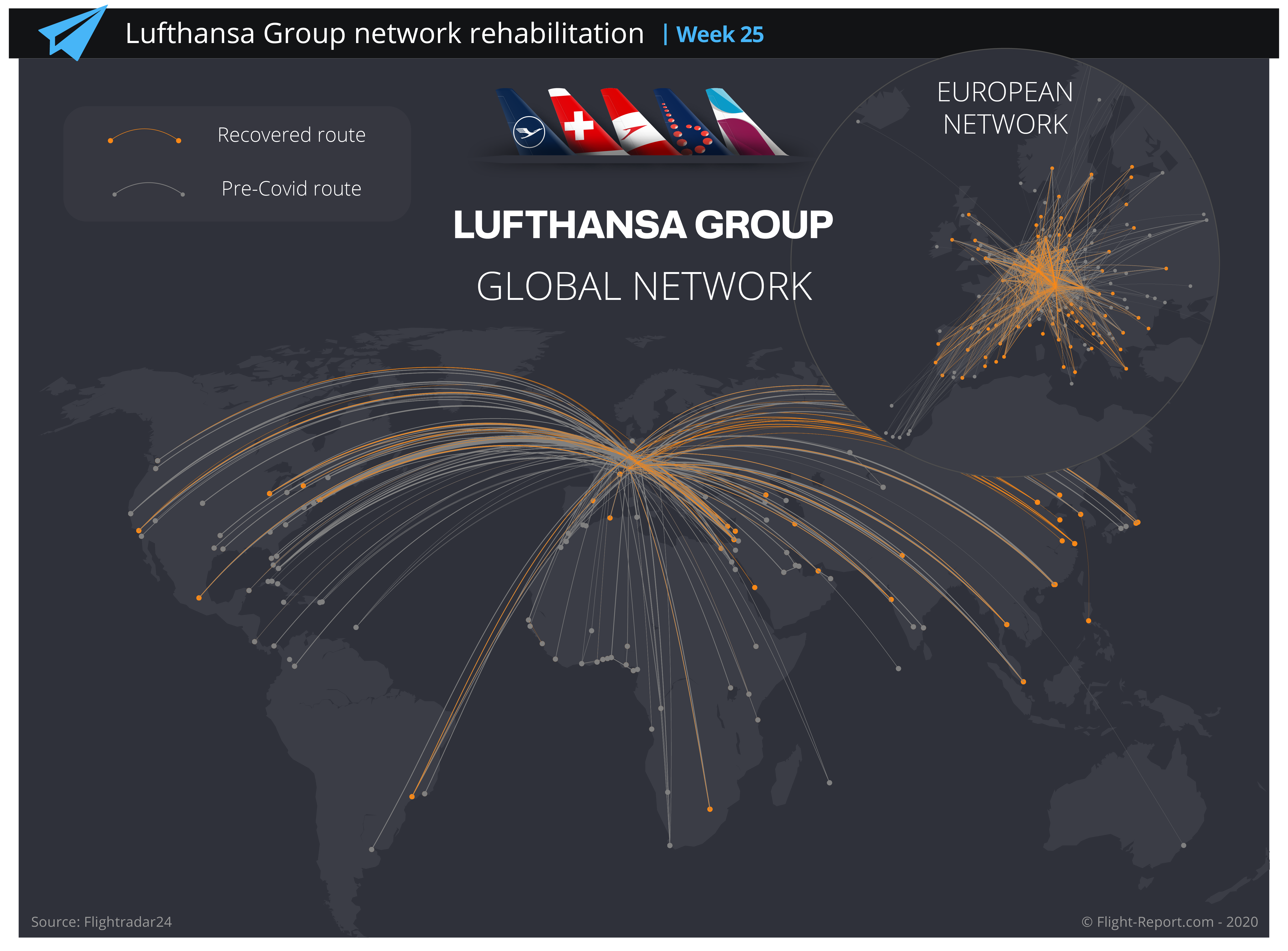

In the past week, with the reopening of some intra-European borders, ramp up has been sensible with double digit growth in a majority of indicators–Air France-KLM being the closest to its pre-Covid profile at this stage. Lufthansa Group has carried out a significant increase in capacity over the past week, while IAG, still highly crippled by quarantine measures in the UK, lags behind.

More airline-by-airline details may be found below:

Low cost airlines may seem slower to recover in each group. Yet, by taking a closer look at the situation we may observe that this is mostly explained by a slower reopening of countries to which LCCs are highly exposed (mainly Spain, where borders have only reopened since last Sunday, hence very marginally captured by this update).

Interestingly, Air France-KLM reduced operations later than peers back in March and has now become the most aggressive player in the recovery at this stage. While Air France is certainly adding more and more flights, KLM has been the main driver of this ramp up, keeping a higher proportion of flights than all its peers since the beginning of the crisis.

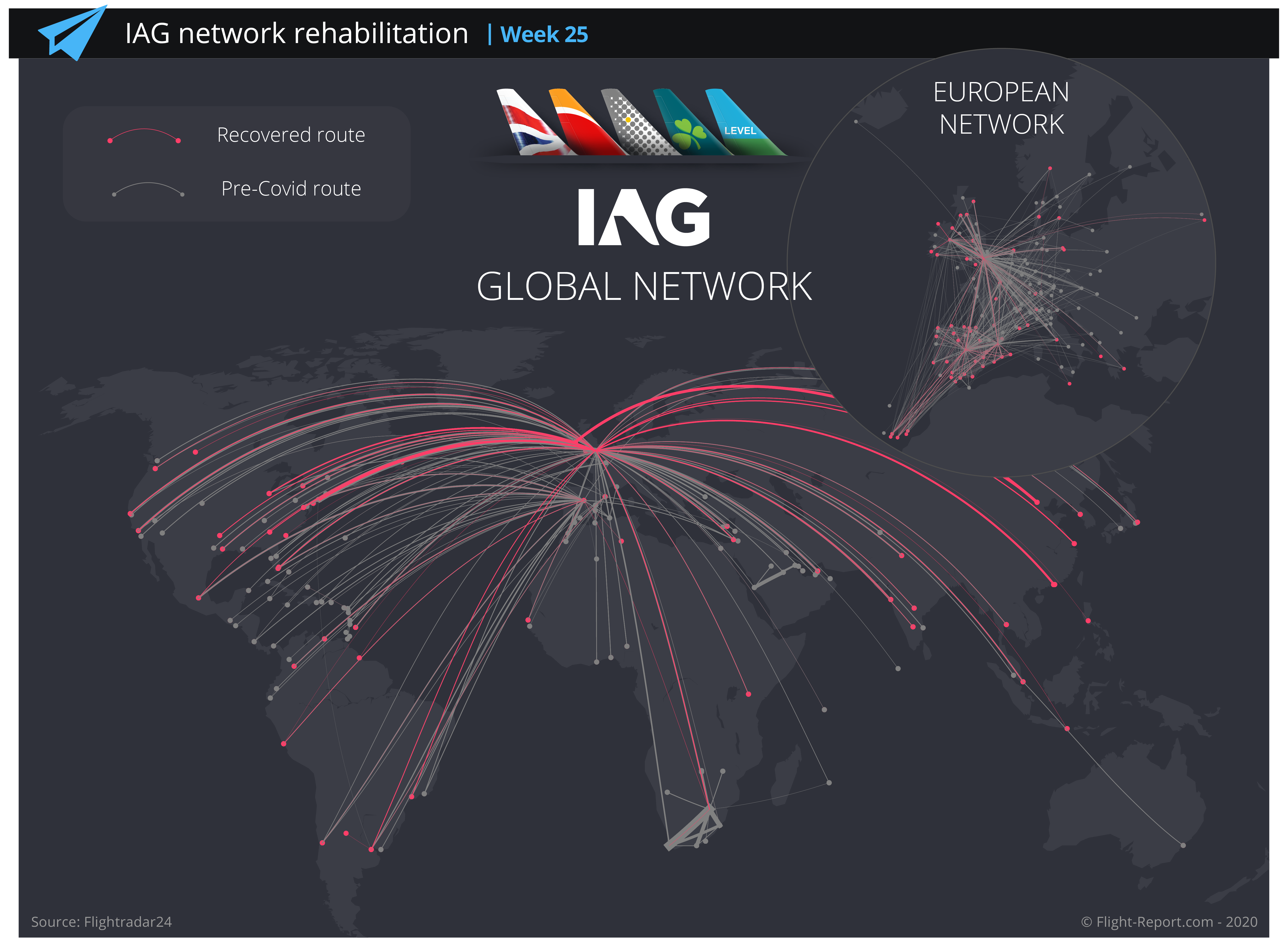

In terms of networks, our maps still show a clear reduction in the number of destinations, especially international routes. Central America and Eastern Europe appear to be regions where the 3 groups are taking longer to come back. Also of note is the much-limited recovery of IAG within Europe compared to its peers (due to aforementioned factors).

Week 25 takeway

In the last week, traffic recovery has been booming for the 3 airline groups, especially in Europe where the end of lockdown measures in many countries, as well the reopening of some borders, have allowed the airlines to operate more routes. Air France-KLM still appears to be the most aggressive, but Lufthansa Group is rapidly catching up. More insights on IAG’s strategy are likely to be seen in the next weeks with political updates expected in the UK.